About me

Hey there! I’m Shihao Zhang 👋, all the way from Shuyang (a tiny, charming city in Jiangsu, China). I’m currently pursuing my Master’s in Operations Research at Columbia University (Go Lions! 🦁), after graduating with a Bachelor’s in Financial Engineering from CUFE. When I’m not buried in work or study, you’ll find me kicking around a soccer ball ⚽—I’m a die-hard fan of both Jiangsu FC and Manchester United (Glory Glory Man United! 🏟️). I also love hitting the slopes 🎿, capturing life through my camera lens 📸, and feeling the wind on a cycling trail 🚴. Lately, I’ve been trying my hand at tennis 🎾 (beware of my serve… it’s a work in progress ).

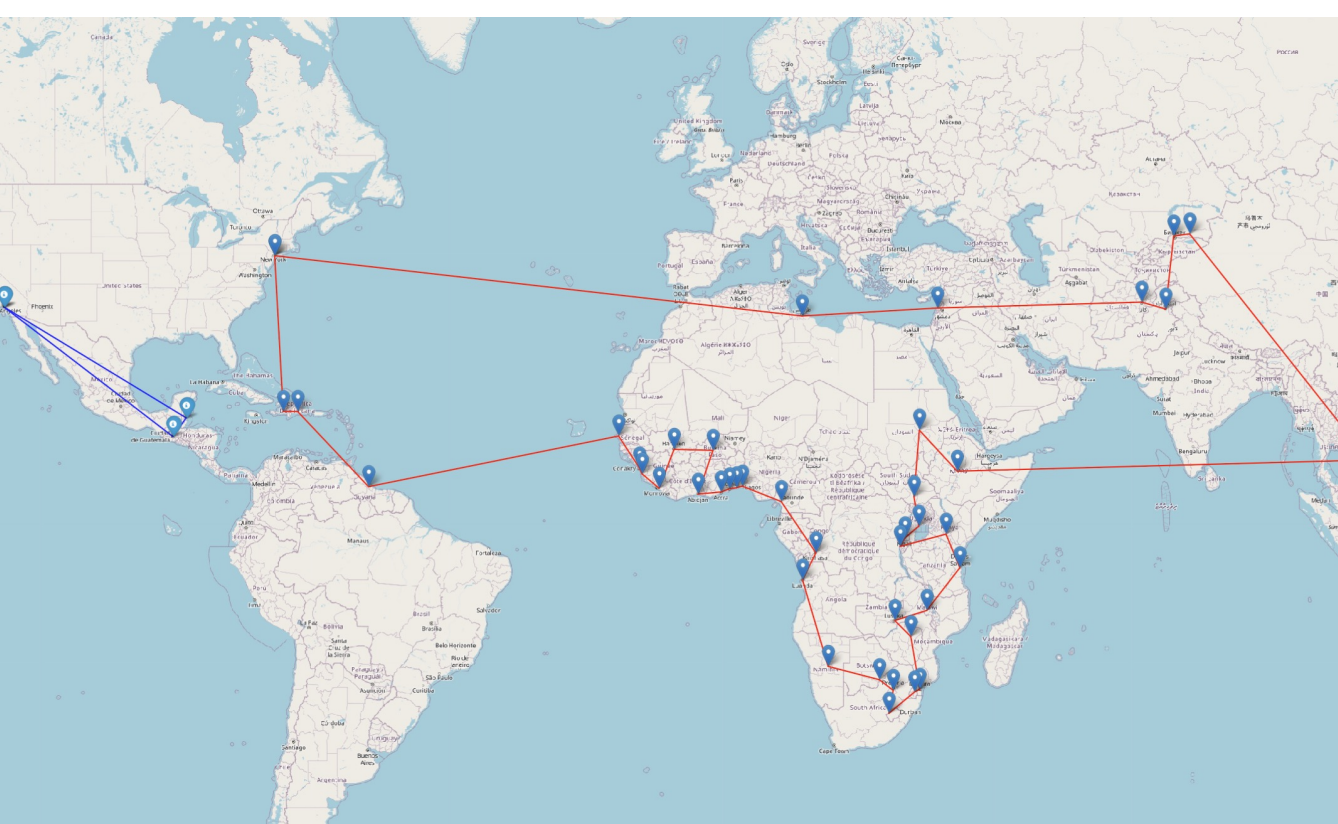

Travel is one of my biggest passions. So far I’ve wandered through almost half of China, and ventured abroad to Japan, USA, UK, Mexico, Belgium and Singapore—each trip adding a new chapter to my story 📚✈️.

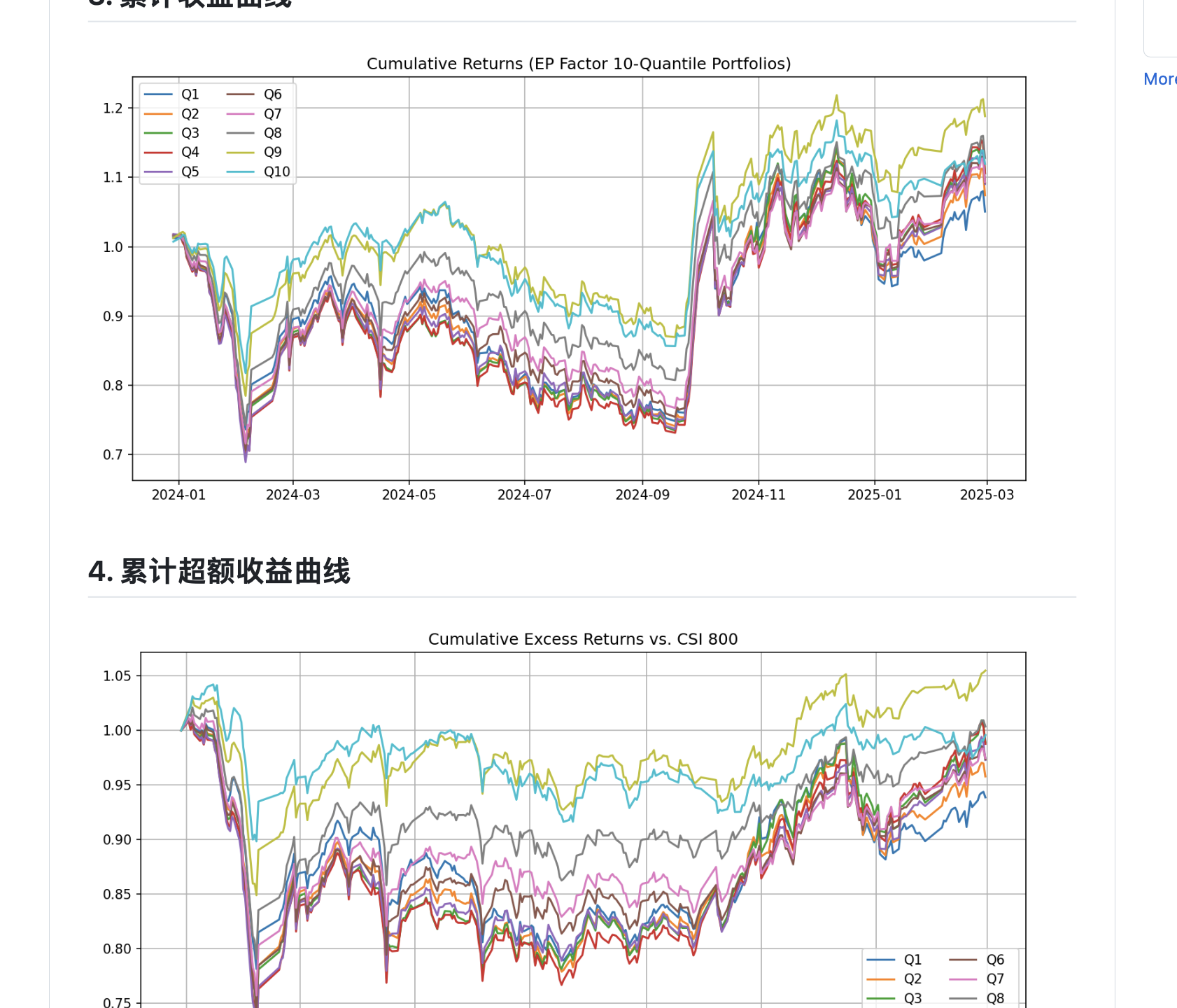

Professionally, I’m all about quantitative finance: I’ve completed several internships focused on factor research, model building, and strategy optimization. 💼✉️ I’m currently exploring PhD opportunities and am deeply interested in quantitative finance, asset pricing, and operations research. If your program has openings or you know of any faculty looking for students in these areas, I’d love to connect! 🎓📊

What i'm doing

-

Quantitative Finance

Building models and optimizing investment strategies in equity markets.

-

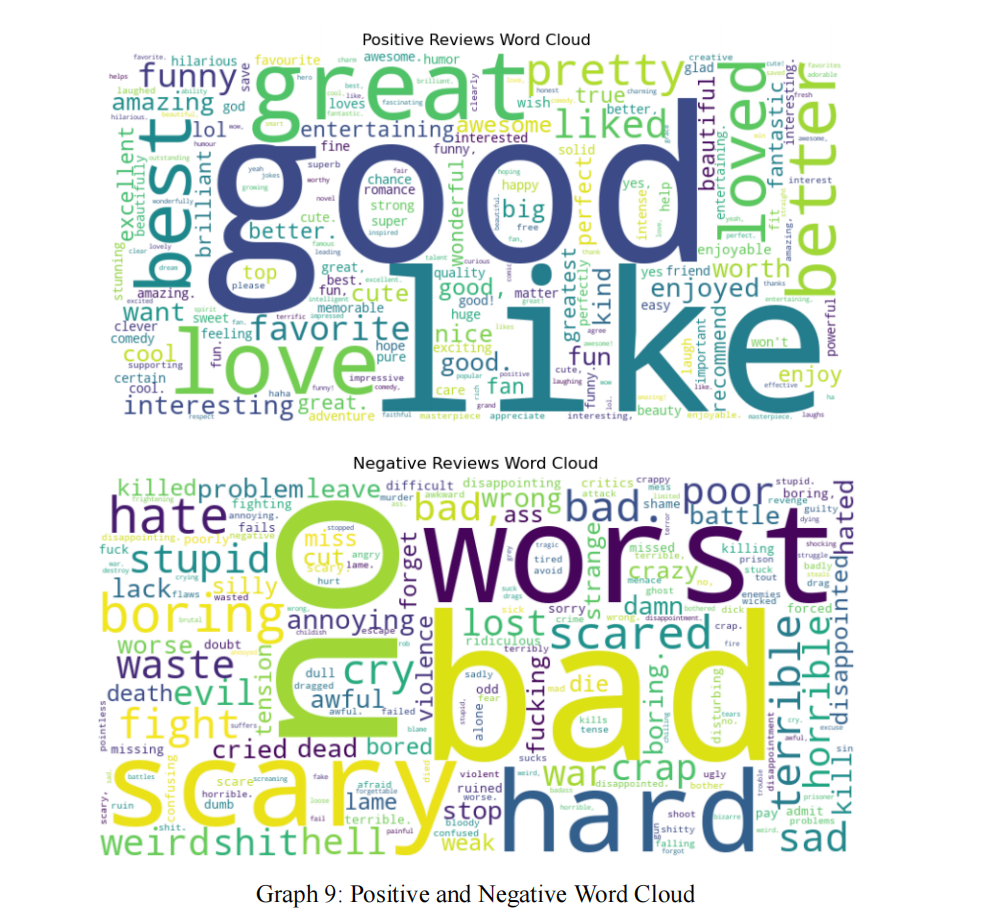

Data Science

Collecting, cleaning, and visualizing data using Python, SQL, and machine learning techniques to uncover actionable insights.

-

Crypto Research

Exploring blockchain protocols and backtesting crypto trading strategies

-

Travel & Outdoor Adventures

Capturing life's moments through my camera—always seeking the next adventure.